We see retail businesses succeed or fail based on the payment infrastructure they choose to deploy. When you run a modern store, speed and reliability mean everything for your bottom line. In a physical environment, a slow card terminal creates long lines and frustrates shoppers, leading to lost immediate revenue. Online, a clunky checkout process leads directly to cart abandonment. You need a partner that handles the heavy lifting of security and settlement instantly.

The best payment processing for retail connects your inventory, syncs your sales data across every channel, and processes funds securely. Furthermore, the differences between in-store and online needs are massive, requiring a specific approach for each. Physical stores need durable hardware and offline modes, while online stores need fast digital wallets and cross-border capabilities. Identifying the best retail payment processing for your specific model is the only way to protect your margins as you scale.

To help you navigate this complex market, we built this practical comparison guide. We evaluate the leading retail payment processing companies so you can build the optimal checkout experience for your shoppers. If you want robust merchant payment solutions to scale your business, you must understand exactly how these systems function. We will explore the market leaders and highlight how a platform like ConnectPay provides advanced financial tools to push your operations forward.

Quick Answer: What Is the Best Payment Processing for Retail?

Finding the right system takes time, but here is our quick breakdown of the retail payment processing companies leading the industry:

- ConnectPay: The best choice for online-first and omnichannel retailers scaling across Europe.

- Square: The ultimate all-in-one POS and payment solution for physical brick-and-mortar stores.

- Stripe: The go-to developer platform for highly customized online retail and complex subscriptions.

- Adyen: The premium choice for massive global enterprises needing unified commerce everywhere.

- Shopify Payments: The most seamless native option for retailers already using the Shopify platform.

Ultimately, identifying the best retail payment processing completely depends on your core business model. You must decide if you operate strictly in-store, purely online, or across a blended omnichannel environment.

Retail Payment Processing Solutions: Comparison

We created this comparison table to summarize the key strengths of these retail payment processing solutions. Comparing these retail payment processing companies side-by-side helps you cut through the marketing noise and focus on the features that actually impact your profit margins.

| Provider | Core Features | Best For | Pricing Model / Fees | Key Advantage |

|---|---|---|---|---|

| ConnectPay | Online payments, APIs, 80+ Currencies | Online-first & omnichannel in Europe | Custom / Volume-based | Compliance & embedded finance |

| Stripe | Custom online checkout, Subscriptions | Tech-driven online retail | Flat-rate + custom | Unmatched developer APIs |

| Worldpay | Global POS hardware, Online gateways | Large international retail chains | Interchange++ | Massive global acquiring |

| Square | POS registers, Inventory syncing | Small to mid-sized physical stores | Flat-rate | Easy all-in-one ecosystem |

| PayPal | Digital wallets, One-click checkout | Small retailers needing fast setup | Flat-rate | Huge consumer brand trust |

| Adyen | Unified omnichannel, Global reach | Enterprise omnichannel retailers | Interchange++ | Single platform global reach |

| Shopify Payments | Native ecommerce, Integrated POS | Shopify-based online retailers | Flat-rate | Seamless platform integration |

7 Best Payment Processing Solutions for Retail

Let’s dive deeper into this curated list of the 7 top retail payment processing services. We cover options for in-store, online, and blended omnichannel needs. Some providers on this list specialize heavily in physical POS hardware, while others – like ConnectPay – excel in online expansion and cross-border ecommerce. These tools represent the best payment processing for retail available today. We evaluate each retail payment processing system based on real-world execution, so start here.

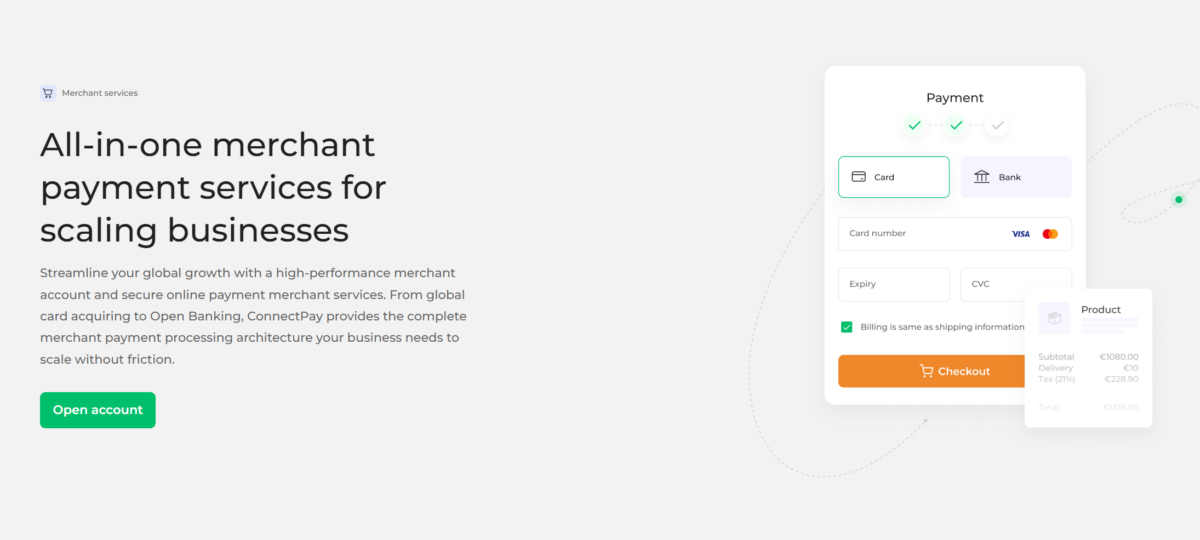

1. ConnectPay

Best for: Online-first and omnichannel retailers in Europe

We built ConnectPay as a fully EMI-licensed platform specifically designed for online and platform-based retail businesses. While many legacy providers just process a credit card, our platform handles the entire financial lifecycle of a modern retailer. We process massive transaction volumes safely across multiple European jurisdictions.

We support 80+ currencies natively, process SEPA and SWIFT transfers flawlessly, and integrate Apple Pay via robust APIs. We handle the strict compliance requirements of GDPR and PSD2 on your behalf. Our built-in KYC/AML protocols verify buyers and vendors instantly, while 3DS and biometric security features stop fraud dead in its tracks. For example, a European marketplace selling local fashion uses our system to accept payments in local currencies and distribute payouts to vendors securely.

Pros:

- Strong Compliance and Security: We handle strict European financial regulations so you can focus on selling.

- Global Reach: We offer true multi-currency support to boost cross-border checkout conversions.

- Advanced Infrastructure: We provide complete embedded finance tools, not just a simple payment gateway.

Cons:

- No Hardware Focus: We do not focus on providing in-store physical POS registers.

- Scale Required: Our advanced APIs are better suited for scaling or online-first retailers rather than a weekend hobby store.

When it comes to retail payment processing, ConnectPay stands out for businesses actively scaling online. We provide the best payment processing for retail platforms looking to expand globally without compliance headaches.

2. Stripe

Best for: Online and omnichannel retailers needing customization

Stripe dominates the market as the developer-first standard for online checkout experiences. We see highly technical retail teams use Stripe to build incredibly customized payment flows. You can mold their APIs to fit any unique retail model imaginable.

Stripe provides a powerful suite of tools, including online checkout pages, subscription billing engines, and connected account logic. They handle complex payment routing effortlessly. For instance, a bespoke retail brand offering monthly subscription boxes uses Stripe to manage recurring billing, failed payment retries, and customer card updates automatically.

Pros:

- Flexible Integrations: You can connect Stripe to thousands of popular inventory and CRM tools.

- Strong Developer Tools: Their documentation makes building custom checkouts highly predictable.

Cons:

- Complexity: You absolutely need a skilled development team to unlock their best features.

- Pricing Transparency: Flat-rate pricing looks simple but eats into margins quickly at high volumes.

Stripe remains one of the top retail payment processing solutions for online stores possessing strong internal technical resources.

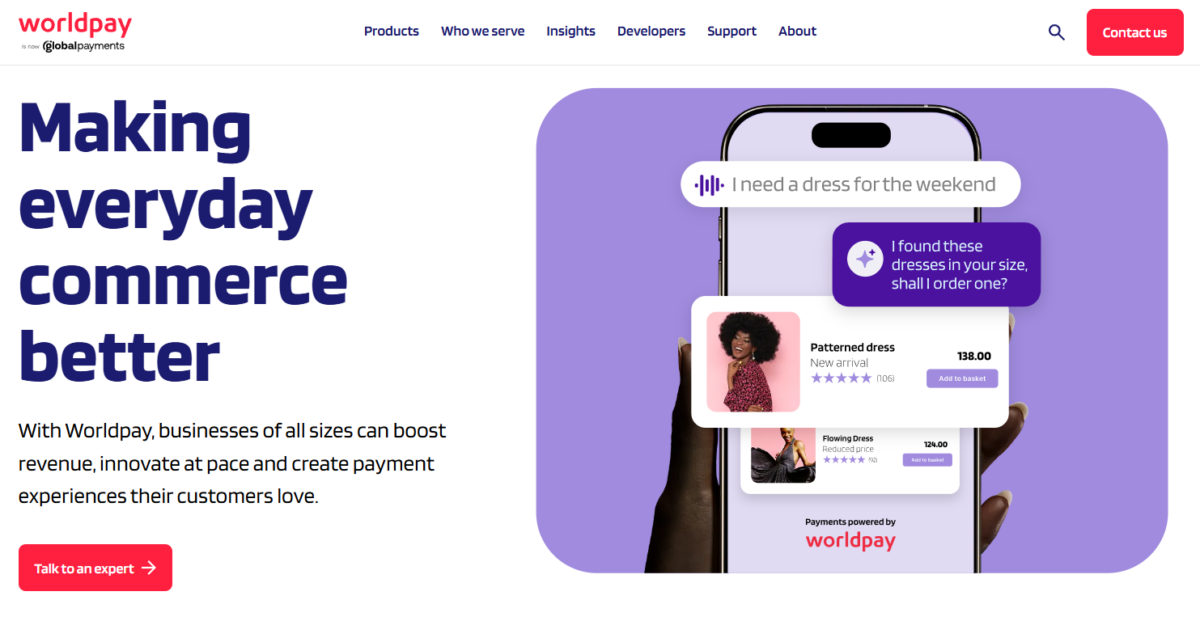

3. Worldpay

Best for: Large retail chains

Worldpay operates as one of the largest and oldest payment processors globally. They cater primarily to massive, established retail chains that process thousands of physical and digital transactions every single hour. We see Worldpay utilized by massive grocery chains and international clothing brands.

They provide traditional global payment processing, massive fleets of physical POS hardware, and highly specialized risk management tools. They negotiate custom interchange-plus rates for massive enterprises, ensuring costs stay low at scale.

Pros:

- Massive Scalability: They handle enterprise-level transaction volumes without breaking a sweat.

- Wide Payment Support: They process nearly every local and international payment method in existence.

Cons:

- Legacy Systems Feel: Their backend software and merchant dashboards feel incredibly clunky and outdated.

- Complex Setup: The corporate onboarding process takes weeks of paperwork and negotiations.

If you want reliable retail payment processing services at an absolute massive global scale, Worldpay is a proven giant.

4. Square

Best for: Small to mid-sized brick-and-mortar retailers

Square completely revolutionized the physical retail environment. We recommend Square for local shops, cafes, and pop-up retailers who need an instant, reliable way to take physical cards. They bridge the gap between physical retail and basic e-commerce brilliantly.

Square offers an all-in-one POS system connected directly to a payment gateway. You purchase their sleek hardware registers, and their software syncs your physical inventory with your online store instantly. For example, if you sell your last sweater in your physical boutique, Square instantly marks it “out of stock” on your website.

Pros:

- Easy Setup: You can create an account, plug in a card reader, and sell on the same day.

- All-in-One Ecosystem: They manage your hardware, software, inventory, and staff payroll in one dashboard.

Cons:

- Limited Scalability: Their flat-rate fees become very expensive as your physical retail footprint grows.

- International Weakness: They offer less robust support for international expansion and cross-border selling.

Square offers the best retail payment processing for businesses heavily focused on local physical foot traffic. It operates as a highly reliable retail payment processing system.

5. PayPal

Best for: Small retailers needing quick online payments

PayPal remains an incredibly powerful tool for consumer trust in the online retail space. We see new retailers use PayPal to instantly legitimize their brand. Shoppers trust the PayPal logo, which drastically reduces cart abandonment for unknown stores.

PayPal provides a globally recognized digital wallet and a fast checkout experience. You integrate their button into your site, and customers bypass entering full credit card details.

Pros:

- Trusted Brand: Consumers feel highly protected using their PayPal accounts to shop.

- Easy to Use: Adding PayPal to any modern ecommerce platform takes just a few clicks.

Cons:

- Higher Fees: Their transaction fees are noticeably higher than standard direct processors.

- Limited Customization: You have very little control over the checkout interface or user experience.

PayPal remains one of the top retail payment processing companies for generating quick, trusted sales.

6. Adyen

Best for: Enterprise omnichannel retailers

Adyen serves as the premium, unified commerce engine for massive enterprise retailers. Brands like H&M and Uber use Adyen to power their global operations. We see Adyen effectively consolidating fragmented international payment systems into one clean, global data stream.

Adyen provides enterprise-grade infrastructure. They offer direct global acquiring, meaning they connect directly to Visa and Mastercard networks to improve authorization rates. They manage both high-end physical POS terminals and global ecommerce checkout pages.

Pros:

- Global Reach: They process transactions efficiently across nearly every continent.

- Unified Commerce: You view your physical store data and online store data in one unified report.

Cons:

- Complex Onboarding: Adyen requires extensive technical resources and corporate compliance checks to launch.

- Expensive Minimums: They generally ignore small businesses and enforce high monthly volume minimums.

Adyen ranks clearly among the best retail payment processing companies for massive global enterprises.

7. Shopify Payments

Best for: Shopify-based online retailers

Shopify Payments represents the absolute path of least resistance if you already run your store on the Shopify platform. We see merchants activate this native tool instantly to avoid third-party gateway configurations.

Powered quietly by Stripe in the background, Shopify Payments handles all standard credit cards and digital wallets natively within your Shopify dashboard. It seamlessly connects with Shopify POS hardware for physical pop-up sales.

Pros:

- Seamless Integration: It is built directly into your store with zero coding required.

- Simplified Setup: You manage payouts, chargebacks, and inventory from the exact same screen.

Cons:

- Platform Lock-in: You cannot use Shopify Payments outside of the Shopify ecosystem.

- Less Flexibility: You lose the granular API control that independent platforms like ConnectPay or Stripe offer.

If you live entirely within the Shopify ecosystem, this is excellent payment processing for retail.

Why Retail Businesses Need the Right Payment Processor

You must understand that choosing a payment processor acts as a fundamental growth decision. A poor processor destroys your conversion rates. We constantly analyze retail checkouts, and we see cart abandonment spike the moment a checkout page loads slowly or looks suspicious. A top-tier retail payment processing platform guarantees fast checkout speeds.

When you expand internationally, the right processor offers local payment methods so foreign buyers can shop comfortably. Furthermore, modern shoppers expect a flawless omnichannel experience. They want to buy an item online and return it smoothly at your physical store. If your physical systems and online systems cannot talk to each other, you create a miserable customer experience. Investing in seamless ecommerce payment processing and reliable in-store hardware ensures you capture every possible sale, protect your profit margins, and keep your retail customers coming back.

How to Choose the Best Retail Payment Processing Solution

Finding the right financial partner requires a strategic approach. You must evaluate how your specific retail model operates daily. A local coffee shop needs entirely different tools than a cross-border fashion marketplace. We use this actionable framework to help teams select the optimal payment processing for retail platforms. By following these steps, you will locate the strongest retail payment processing solutions for your unique operations.

In-Store vs Online vs Omnichannel Needs

First, accurately define your sales environment. If you sell 100% of your products in a physical brick-and-mortar location, you need durable POS hardware, offline payment modes, and integrated receipt printers. If you sell exclusively online, you need robust digital wallets, high-speed APIs, and multi-currency tools. If you run an omnichannel retail operation, you absolutely require a unified system that synchronizes physical and digital inventory instantly. We highly recommend exploring online banking for retail integrations to manage these complex cash flows efficiently.

Fees and Pricing Structures

You must aggressively analyze how a provider structures their fees because these costs eat directly into your retail margins. Evaluate if they charge a simple flat rate or a complex interchange-plus model. Calculate the hidden costs of monthly software subscriptions and international surcharge fees. If you run a subscription box retail model, you must ensure the provider integrates easily with your recurring payment software without triggering massive recurring transaction penalties.

Hardware and Software Requirements

Evaluate the physical and digital tools you must implement. For physical retail, review the cost of card readers, cash drawers, and barcode scanners. Do they force you to buy proprietary hardware, or can you use third-party iPads? For digital retail, check the API documentation. Make sure the processor acts as a frictionless payment gateway that integrates cleanly into your specific e-commerce platform (like Magento, WooCommerce, or Custom React).

Security and Compliance

You cannot ignore security. Retailers act as prime targets for fraudsters. Your processor must handle PCI DSS compliance completely on your behalf. They must offer active fraud protection tools, biometric 3D Secure authentication, and strong encryption data tokenization. For European retailers, GDPR compliance remains absolutely mandatory. Finding a partner that offers embedded compliance saves your legal team hundreds of hours and protects your brand from devastating financial fines.

Common Retail Payment Processing Fees Explained

Understanding your monthly billing statement protects your profit margins. We see retail teams lose significant capital simply because they do not understand the fee structure they signed up for. Every retail payment processing provider has a different way of extracting revenue from your sales.

We recommend paying close attention to cross-border costs. If you process high volumes of euro-zone payments, you need transparent FX rates. Furthermore, if you manage a marketplace with multiple retail vendors, you absolutely need efficient, low-cost best bulk payment solutions to handle mass payouts without losing your shirt to wire fees.

Transaction Fees

This forms the core cost of doing retail business. Every single time a customer taps a card or clicks “buy,” the processor takes a specific cut. This typically involves a percentage of the total sale volume plus a fixed flat fee (for example, 2.9% + $0.30 per successful charge). You must check if your provider uses “flat-rate pricing” (simple to read but expensive at scale) or “interchange-plus pricing” (harder to reconcile but vastly cheaper for high retail volumes).

Hardware and Setup Costs

If you operate physical retail locations, you must purchase physical terminals. Some processors give you a basic swiper for free but charge hundreds of dollars for advanced register screens, receipt printers, and barcode scanners. Look closely at hardware warranties and whether the software running on the POS terminal requires a separate monthly subscription fee per retail location.

Hidden Fees and Chargebacks

If a customer disputes a charge with their bank (claiming fraud or a broken item), the provider hits you with a steep chargeback fee (often ranging from $15 to $25), and you pay this penalty even if you eventually win the dispute. You must also watch out carefully for hidden contractual costs like monthly gateway access fees, recurring PCI compliance fees, or massive early termination penalties if you try to leave the contract early.

Ready to Upgrade Your Retail Payments?

As your retail brand scales, outgrowing your initial, basic payment terminal is a natural sign of success. To successfully capture global markets and aggressively protect your profit margins from rising fees, you must adopt scalable, modern payment solutions. The best payment processing for retail platforms do much more than just authorize a basic credit card; they offer full, embedded financial infrastructure to support your entire omnichannel operation.

We built ConnectPay specifically as a future-ready, compliant option for growing online and expanding retail businesses. From handling complex multi-currency accounts to offering deep compliance and global reach, we give you the backend engineering power to scale without limits. If you want to stop losing money on bad checkout flows and high cross-border fees, it is time for a massive upgrade. Visit https://connectpay.com/ today to discuss how we can implement powerful embedded finance tools to upgrade your retail payment processing and streamline your operations.

FAQs: Retail Payment Processing Solutions

What is the best payment processing for retail businesses?

The best provider depends on your exact retail channel. ConnectPay is the top choice for online-first platforms scaling in Europe. Square dominates for small physical brick-and-mortar stores. Adyen serves massive global enterprise retailers with unified commerce needs.

What fees do retail payment processors charge?

Retail processors typically charge a transaction fee per sale (usually a percentage plus a flat rate like 2.9% + $0.30). You also face physical hardware costs for in-store sales, monthly gateway fees, chargeback penalty fees, and currency conversion fees for international transactions.

Which payment processor is best for small retail stores?

Square represents the absolute best option for small physical retail stores. They offer easy-to-use physical card readers, no monthly fees, flat-rate pricing, and an intuitive inventory management dashboard that syncs seamlessly with a free online store builder.

Can retail businesses accept international payments?

Yes. Modern online retailers can accept international payments easily. However, you must choose a processor like ConnectPay, Checkout.com, or Adyen that offers strong multi-currency support and smart local routing to avoid massive foreign exchange fees and high decline rates.

What is the difference between POS and online payment processing?

POS (Point of Sale) processing involves physical hardware terminals used to swipe, dip, or tap cards in a physical retail store. Online payment processing utilizes secure digital gateways and APIs to authorize digital card entries and e-wallets on a website or mobile app.

How do I switch retail payment processors?

To switch safely, you first set up and verify your new merchant account. You order new physical terminals or install the new digital API integration. Finally, you safely migrate your customer token data (ensuring strict PCI compliance) and run thorough tests before turning off your old provider.